In 2015, China's automotive power lithium-ion battery was in a state of great excitement. This has been remarkable in both the market and industry.

1.1 Market development status

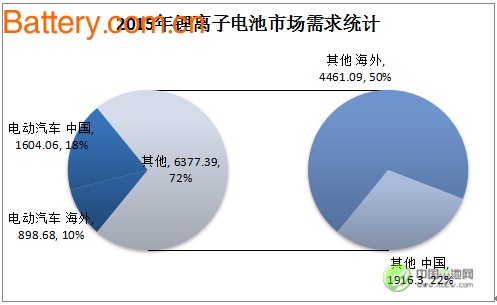

According to the data of the real lithium research, the total demand for lithium-ion batteries in the Chinese market in 2015 reached 35.236 million kWh, an increase of 79.08% year-on-year; the global market share reached a new high of 39.64%, an increase of more than 10 percentage points over 2014. Among them, the demand for lithium-ion batteries in the fast-growing China's new energy vehicle market is as high as 160.4060 million kWh (excluding the demand for imported vehicles), up nearly 300% year-on-year; accounting for 45.57% of the total demand for lithium-ion batteries in the Chinese market. Compared with 21.42% in 2014, it has more than doubled.

More than three-quarters of the increase in demand for lithium-ion batteries in the Chinese market in 2015 was created by the new energy vehicle market. In 2015, the total demand for global automotive power lithium-ion batteries was 2,502,740 kWh, and 64.09% was contributed by the Chinese market.

Figure 1. Demand statistics for lithium-ion batteries in the global and Chinese markets in 2015 (unit: 10,000 kWh)

According to statistics from the Ministry of Industry and Information Technology, in 2015, Chinese car companies produced a total of 379,018 new energy vehicles, and the lithium research deducted vehicles that did not use lithium-ion batteries (mainly lead-acid batteries, nickel-metal hydride batteries and supercapacitors ). After the fuel cell vehicle, there were 355,891 vehicles remaining. Among them, there are 137,621 pure electric passenger cars, 3.531 million kWh for lithium-ion batteries, 63,048 for plug-in hybrid passenger cars, 902,200 kWh for lithium-ion batteries, and 85,517 for pure electric buses. Lithium-ion battery demand is 926.17 million kWh; plug-in hybrid bus 23,770, lithium-ion battery demand 635,500 kWh; pure electric special vehicle 45,935, lithium-ion battery demand 1.7096 million kWh.

The new energy vehicle market has become the most important driving force for the rapid development of China's lithium battery industry, and the main reason for the new leap in the new energy vehicle market is the high subsidy policy of the Chinese government. The total subsidy for the two-tier government (central + local) of some models even covers the full cost of the vehicle. For example, a 16- to 8-meter pure electric bus, the total subsidy of the two levels of government can be up to 600,000 yuan / vehicle, and the full cost of the vehicle will not exceed 500,000 yuan / vehicle; 2 A00-class micro-pure electric ride with a cruising range of more than 150km With the car, the two-level government subsidies can reach up to 70,000 yuan per vehicle, and the total cost of the vehicle is almost 70,000 yuan per vehicle. In the case of these two types of new energy vehicles, the government has actually become the ultimate buyer. In the total sales of domestic new energy vehicles in 2015, the sales of these two types of vehicles accounted for a high proportion of nearly 40%.

The price level of power battery in China's new energy automobile market in 2015: the price of battery products is about 1,600 yuan/kWh (cost is about 1,200 yuan/kWh), and the price of battery packs is mostly at 2,400-2,500 yuan/kWh. Between (cost about 1,800 ~ 1,900 yuan / kWh).

1.2 Status of industrial development

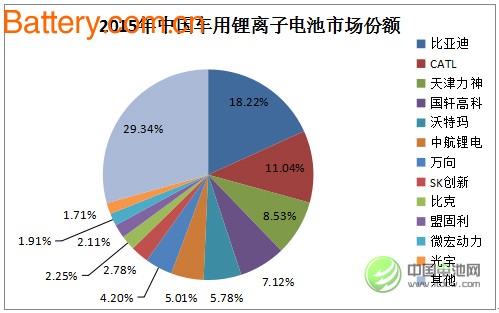

Corresponding to the rapid development of the market, the industry is also developing at a high speed. In the impression of True Lithium Research, before the 2008 Beijing Olympic Games, only the companies engaged in the development of automotive-powered lithium-ion battery technology were CITIC Guoan Mengli and Wanxiang. After the success of the scale trial operation of 50 electric buses in the Beijing Olympic Games, the Ministry of Science and Technology launched the “Ten Cities and Thousand Vehicles†program in early 2009, and the country began to pay attention to the development of new energy vehicles. After that, the number of battery companies developing the market for lithium-ion battery for vehicles began to increase, and it began to break out after 2013. In 2015, China's new energy vehicle market has the number of companies supplying power batteries. The statistics of True Lithium Research show up to 120 (including a small number of module suppliers), while at the same time, there are no more than 10 overseas markets. China is obviously overheated.

Figure 2. Statistics of various companies in China's automotive lithium-ion battery market in 2015 (Note: refers to battery companies)

Although there are many suppliers of automotive power lithium-ion batteries, the market is relatively concentrated in the hands of a few manufacturers. As shown in Figure 2, the market share of the 12 battery manufacturers in Figure 2 totaled more than 70%, of which the five manufacturers of BYD, CATL, Tianjin Lishen, Guoxuan Hi-Tech and Waterma had a combined market share of more than 50%. Decentralization is also concentrated, which is the biggest feature of China's automotive power lithium-ion battery market in 2015.

BYD battery has become the largest supplier of automotive power lithium-ion batteries in China with a supply of 2,292,400 kWh in 2015, with a market share of 18.22%. It mainly supplies BYD Auto and its associated car companies (BYD-Daimler and Tianjin Bus). CATL is ranked second with 1,771,600 kWh, and more than 90% of its products are supplied to the new energy bus market, of which more than 60% are supplied to Yutong Bus, and have not yet entered the electric special vehicle market. Tianjin Lishen ranked third with 1,367,600 kWh, focusing on the pure electric vehicle market, and customers are more dispersed. More than 80% of Guoxuan Hi-Tech's products supply the pure electric bus market, while Waterma is the largest power battery supplier in the electric special-purpose vehicle market.

Due to the ambiguity of the policy (the policy only requires the power battery to be made in China, it is not clear whether the module is made in China or the battery is made in China), the battery products of the Korean battery giant entered the Chinese new energy vehicle market in 2015. SK Innovative, LG Chem and Samsung SDI, the three Korean manufacturers in 2015 supplied a total of 197,160 kWh of battery products to the Chinese market. Among them, SK's innovative 445,600 kWh batteries were all supplied to Beijing Electric Controls in the form of imports. Sikai, LG Chem and Samsung SDI have some batteries that are supplied to domestic module manufacturers in an imported way, mainly 18650 batteries. In addition, Japan's major manufacturers Panasonic and AESC also have a small number of battery products to be supplied to domestic module manufacturers.

Table 1: Major Manufacturers' Customer Relationship in China's New Energy Vehicle Market in 2015

Note: Only refers to the battery supply.

2015 China's new energy vehicle market power battery manufacturing cost level: battery product cost is about 1,200 yuan / kWh (BYD minimum, about 1,100 yuan / kWh), the battery composition is mostly at 1,800 yuan / kWh .

Application Status of China's Automotive Power Lithium Ion Battery Products in 2015

1.3 Status of product demand

From the perspective of the cathode material used, the battery core is mainly divided into two series of lithium iron phosphate and ternary/manganese acid. In theory, the lithium iron phosphate power battery has a slightly lower energy density but relatively better safety, and the ternary/lithium manganate power battery is just the opposite. In China's new energy vehicle market in 2015, the demand for power supply of ternary/lithium manganate series is much higher than that of lithium iron phosphate power batteries. According to the data of the real lithium research, the demand for ternary/lithium manganate power batteries in 2015 was 4,411.6 thousand kWh, which was an astonishing 882.111% compared with 449,200 kWh in 2014. At the same time, lithium iron phosphate battery The demand was 1,162,890 kWh, an increase of 225.86% over the 3.586 million kWh in 2014.

In 2015, ternary/lithium manganate power battery applications showed rapid growth in various markets, among which the electric special vehicle market grew fastest, but it was the largest in the electric passenger vehicle market. As shown in Table 2, the demand for ternary/manganese acid lithium battery in China's electric special vehicle market reached 873,500 kWh in 2015, which is more than 40 times that of 22,000 kWh in 2014; the demand for electric passenger vehicle market It reached 1.944 million kWh, which was 10.7 times that of 2014's 181,600 kWh. Among them, the consumption of ternary/lithium manganate power battery in pure electric passenger vehicle has exceeded 50%, and most of the major car companies such as Zhongtai and Beiqi are pure. Electric passenger car products have adopted ternary/lithium manganate power batteries in 2015.

In the 2015 new energy automobile market in China, the total demand for lithium iron phosphate power batteries was as high as 14,142,200 kWh, and the market share was as high as 71.20%. Among the lithium iron phosphate power batteries, another 70.89% is used in the electric bus market, especially in the pure electric bus market. The market demand is as high as 8,075,700 kWh (including lithium iron phosphate + lithium titanate power battery). The ban on the use of ternary batteries for electric buses was announced in early 2016 and did not affect the market in 2015. In 2015, the ternaryization of the vehicle power battery in the electric bus market is still relatively fast. It is the annual ternary/manganese lithium battery power battery with a consumption of 1,119,600 kWh (including “ternary + lithium titanate†power battery), In 2014, it was 6.35 times of 188,900 kWh.

Due to the special support of the policy, the demand for lithium-ion battery with lithium titanate for negative electrode materials also appeared in the blowout phenomenon in 2015. The annual demand for lithium titanate battery is as high as 513,700 kWh, which is 10 times that of 2014. However, due to the low energy density of the battery, lithium titanate batteries are mainly used in the large electric passenger car market, and have not been applied in the field of smaller electric passenger cars and electric special vehicles.

Table 2: China's new energy vehicle market in 2015, the demand for electricity cells: 10,000 kWh

In terms of cell shape, lithium-ion batteries can be roughly divided into three types: square, cylindrical and soft-packed polymers. In 2015, China's new energy vehicle market, the demand for cylindrical power battery growth is the fastest, which is a total of 3.362 million kWh demand, compared with 694,400 kWh in 2014, the growth rate is as high as 384.29%; The market share of the automotive battery market also increased from 17.28% in 2014 to 20.96% in 2015. At the same time, the application field of cylindrical batteries has also been greatly expanded. In 2014, almost all of them were used in the pure electric bus market, and in 2015, pure electric vehicles. The market for passenger cars and pure electric vehicles has also been used from scratch and has achieved a large number of applications (all of which exceed 800,000 kWh).

In 2015, China's new energy auto market is selling three types of cylindrical power battery products: 32650, 26650 and 18650. (Note: the first two digits of the five digits of the product model refer to the diameter mm, and the middle two refer to the height mm. The last 0 refers to the circle), of which 32650 type products are 926,600 kWh, mainly supplied by Waterma, accounting for 27.55% of the total demand for cylindrical batteries of 3.362 million kWh; the 26650 type products are 94,700 kWh, mainly Suzhou Yuliang is in supply, accounting for 2.82%; the rest are 18650 products, accounting for nearly 70%, and many suppliers.

Square-type power batteries have always been the main products of China's new energy vehicle market, and most of the major manufacturers have taken this path. In the automotive power battery market in China in 2015, the demand for square batteries reached 99.218 million kWh, which is 300.18% higher than the 2.479 million kWh in 2014. However, the market share of 61.85% is roughly equivalent to 61.70% in 2014. . As for the soft-pack polymer battery, although the demand for 27.560 million kWh in 2015 is also large, up 226.46% year-on-year, the market share has declined to some extent: from 21.01% in 2014 to 17.18% in 2015.

In general, the main advantage of cylindrical batteries is that the product consistency is relatively good, the product price is relatively cheap (caused by the higher degree of automation of production), the main problem is that the battery pack contains a large number of batteries, the module capacity The requirements are higher. The advantages and disadvantages of square batteries and soft pack polymer batteries are the opposite of those of cylindrical batteries. It should be mentioned that since the 18650 cylindrical battery has a large number of applications in the consumer electronics market and the small power battery market (such as electric bicycles, power tools, etc.), some battery manufacturers are considering reducing costs or increasing the value of recycling. The cylindrical batteries used in the new energy automobile market are produced on the same platform as the cylindrical batteries used in these markets, and even the same production process is adopted, and the safety hazards caused by this cannot be ignored.

1.4 Battery product supply status 1 (by battery type)

Still the same as above, from the battery type and product form. The lithium titanate battery is also listed separately in terms of battery type. Lithium titanate battery market At present, Weihong Power and Zhuhai Yinlong are in an absolute monopoly position, occupying more than 99% market share in 2015. In addition to these two companies, as well as Anhui days Kang, Sichuan-energy, MGL and other companies are also actively developing lithium titanate battery market, there are a few products on the market. However, in this market segment, Weihong Power and Zhuhai Yinlong's years of hard work and accumulated brand reputation and technical capabilities may make it difficult for other battery manufacturers to look back. Gree Group's 13 billion yuan price to buy Zhuhai Yinlong, it is this fancy.

The main contradiction in the further development of new energy vehicles is that the battery energy density is not high enough to meet the demand. Since the energy density of the lithium titanate battery is significantly lower than that of the battery using the carbon-based anode material, the theoretical space for improvement is not large, and therefore, despite the advantages of long life, high safety, high power charge and discharge, it is destined It will only be a niche market and it will be difficult to become a mainstream battery product in the new energy vehicle market. Coupled with the monopoly pattern of the market has been formed, it is not easy to squeeze in, most battery manufacturers still focus on the carbon-based anode material route. Under the premise that the negative electrode is determined to be a carbon-based material, the main choice of the positive electrode is lithium iron phosphate or ternary/manganese.

The lithium iron phosphate route is a one-sided selection of power battery routes when China began to develop new energy vehicles. It has a solid development foundation in the Chinese market. Many battery manufacturers have clearly focused on developing lithium iron phosphate power battery technology. 12 batteries in Figure 2 Eight of the manufacturers are like this. The power battery products supplied by BYD, Guoxuan Hi-Tech and Waterma to the market in 2015 are all lithium iron phosphate batteries; more than 90% of CATL, AVIC Lithium and Coslight are lithium iron phosphate batteries; 90% of the universal direction is lithium iron phosphate Battery; only Tianjin Lishen turned slightly faster, and the proportion of ternary batteries exceeded 27%. BAK has basically completed the transformation. Of the power battery products supplied to the market in 2015, less than 1% of the products are lithium iron phosphate batteries. Meng Gu Li has been insisting on the ternary/lithium manganate power battery route for many years.

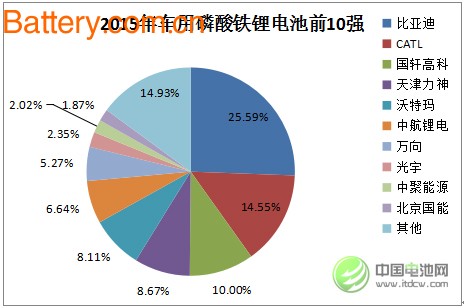

According to data from True Lithium Research, a total of 63 battery manufacturers supplied 14,142,200 kWh of lithium iron phosphate power battery products to the new energy vehicle market in 2015 (only for batteries, excluding lithium iron phosphate batteries using lithium titanate) Among them, the top 10 accounted for more than 85% of the market share, as shown in Figure 3. BYD, CATL and Guoxuan Hi-Tech occupy the top three markets, which are roughly 3 million kWh, 2 million kWh and 1 million kWh respectively. The total market share of the three companies has exceeded 50%, and the oligopoly status has already formed. Manufacturers with a market share of more than 5% include Tianjin Lishen, Waterma, AVIC Lithium and Wanxiang, all of which have supplied more than 600,000 kWh.

Figure 3. Top 10 companies in China's automotive lithium iron phosphate battery market in 2015 (Note: refers to battery companies)

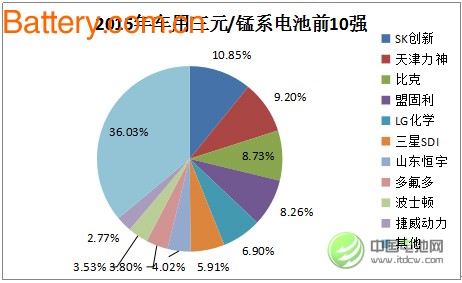

Figure 4. Top 10 of China's ternary/manganese power battery market for vehicles in 2015 (Note: refers to battery companies)

For China's new energy vehicle market, the rise of the ternary/manganese lithium battery line is the last two or three years. Under the guidance of the country's policy, more and more manufacturers have joined the team. In 2015, a total of 44 battery manufacturers supplied 415,560 kWh of ternary/lithium manganate power battery products to the new energy vehicle market (excluding ternary batteries using lithium titanate), of which the top 10 accounted for less than With a market share of 64%, the market concentration is obviously less than that of lithium iron phosphate. The market is still not worthy of the oligarchs. The top ranked is the Korean manufacturer SK Innovation, which cooperates with BAIC New Energy and Beijing Electric Control, with a market share of 10.85%. Two other Korean manufacturers, LG Chem and Samsung SDI, also entered the top 10 list.

Tianjin Lishen, BAK and Menggu Li, three Chinese old-fashioned lithium-ion battery manufacturers ranked second to fourth in the 2015 ternary/lithium manganate power battery supply list, 2015 ternary/manganic acid The supply of lithium-based power batteries has exceeded 300,000 kWh, and their respective market shares are shown in Figure 4. The rising star Shandong Hengyu and Polyfluoride have developed very fast. In 2014, they began to emerge, and in 2015, the annual sales volume was above 150,000 kWh. After Boston Power was acquired by Jinshajiang Capital, it concentrated on developing China's new energy vehicle market and achieved good results. The soft-battery battery flag character Guo Chuntai created the mega-power battery products of Jiewei Power, which has been recognized by Chery and other car companies. The sales volume has risen sharply, and it has ranked among the top 10 in 2015 with more than 110,000 kWh.

Due to the cooperation with BMW (China) Co., CATL has determined that the ternary/lithium manganate power battery is mainly used in the electric passenger vehicle market, and the related progress is also very fast. In 2015, CATL's ternary power battery sales have also been Break through the 100,000 kWh mark. In addition, in 2015, the sales of ternary power batteries for vehicles were above 50,000 kWh, including Foster, Suzhou Xingheng, Suzhou Yuliang, Gushen Energy, Jiangsu Tianpeng, Zhejiang Tianneng, Hunan Sandun, Wanxiang, Jiangsu. Zhihang, Suzhou New Medium Enterprise, among which there are both old and new enterprises, showing the development trend of “Hundred Flowers Blossoming and Hundred Schools of Contentionâ€.

1.5 Battery product supply status 2 (according to product form)

At the beginning of the development of automotive power battery technology, most Chinese manufacturers chose square-type battery routes. Therefore, this route has developed the most mature and has the highest industrial concentration. As shown in Figure 5, in the total demand of 920.18 million kWh of square batteries in 2015, BYD, CATL (formerly ATL Power Battery Division), Guoxuan Hi-Tech, Tianjin Lishen, and AVIC Lithium-Ion (the AVIC lithium battery is a bit special, products The form is a combination of soft pack and square type. These five manufacturers occupy a market share of 76.44% and are in the first echelon; the BYD family accounts for nearly 30% of the market.

Wanxiang, Guangyu, Zhongju, Shandong Weineng, Jiangsu Chunlan, Shandong Hengyuan, Shanghai Aerospace Power, Suzhou Xingheng, etc. are in the second echelon. These manufacturers have a clear gap with the first echelon manufacturers, but the annual sales are more than 100,000 kWh. In addition to the above 13 manufacturers, there are 38 manufacturers with a square power battery supply market in 2015, but these manufacturers have a combined market share of only 8.17%.

Figure 5. China's top 10 automotive battery market in 2015 (Note: refers to battery companies)

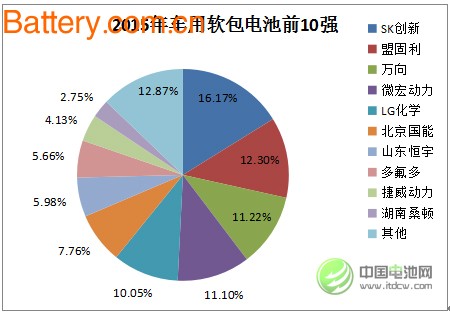

Figure 6. Top 10 of China's automotive soft pack power battery market in 2015 (Note: refers to battery companies)

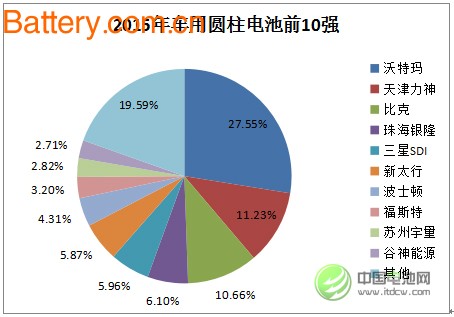

Figure 7. Top 10 Chinese automotive cylindrical battery market in 2015 (Note: refers to battery companies)

Chinese manufacturers' soft-package power battery routes are actually very early, but so far, there are not many manufacturers taking this route. In 2015, only 24 manufacturers had product supply, mainly because the manufacturing cost of soft-pack batteries is relatively high. . The participation of fewer manufacturers has also led to a higher degree of industrial concentration in this route, with the market share of the top 5 manufacturers exceeding 60%.

Before the rise of Tesla , no battery manufacturers considered adopting cylindrical batteries on new energy vehicles. The main concern was safety. After Tesla solved the security problem from the outside of the battery with the superior IT technology of Silicon Valley in California, this route began to be popular around the world, and lithium battery giants such as LG Chem and Samsung SDI participated in it. As more and more Silicon Valley returnees (especially Chinese engineers who have participated in the development of Tesla module technology) return to China to start a business or join a battery factory, the development of modules using 18650-type cylindrical batteries has made the Chinese market rapidly emerge. Batch development of cylindrical power battery manufacturers. In 2015, 34 manufacturers of cylindrical products were applied in China's new energy vehicle market.

Among the 10 manufacturers in Figure 7, except for Watmar, Suzhou Yuliang, Xintaihang, Zhuhai Yinlong and Boston Power, the other five cylindrical power battery products are all 18650 models. Among them, Waterma is the only one with a market share of 27.55% with a supply of 926,600 kWh. Although Samsung SDI built a square-type power battery production base in Xi'an and officially put into operation in October 2015, more than 80% of its products for the Chinese new energy vehicle market in 2015 were cylindrical batteries. It is reported that this is mainly due to China. Driven by car companies and module manufacturers. The remaining 24 manufacturers that did not enter the top 10 are also 18650 models.

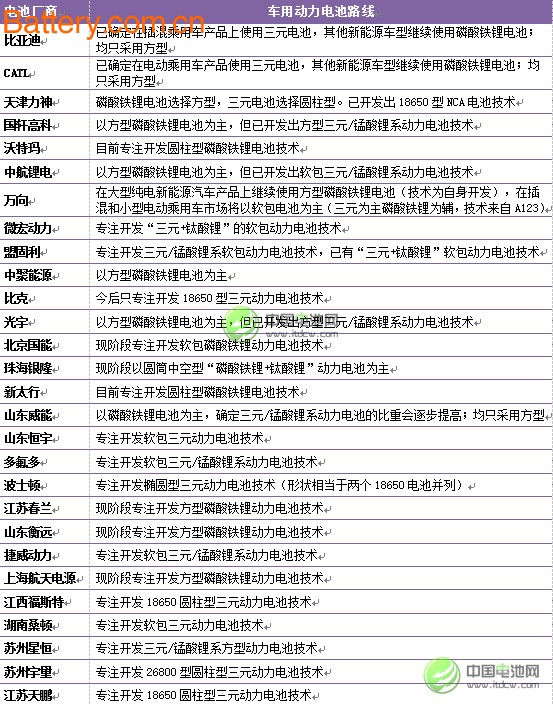

The battery routes of the main power battery manufacturers in China's new energy vehicle market are shown in Table 3:

Table 3: Battery routes of major battery manufacturers in China's new energy vehicle market

Note: China production bases that do not contain foreign manufacturers.

Unfinished~

Shower Cap Machine

1.This machine can produce disposable dust-proof non-woven strip caps of non-woven materials and plastic film materials. This machine has the advantages of good quality, low price and high output, saving labor and reducing costs. It can be customized according to customer requirements.

2.Directly out of the finished product at one time.

3.Automatic constant temperature control.

4.Ultrasonic welding combined with electric heating to make the product more comfortable and firm.

5. The main components are made of aluminum to make the machine lighter and smoother

Shower Cap Machine,Shower Cap Making Machine,Show Cap Machine,Automatic Show Cap Making Machine

Wenzhou Xinlei Machinery Co. Ltd , https://www.xinleimachinery.com